It's a volatile week to be in the Oakville market. The geopolitical shockwaves from the U.S.–Iran conflict have reached our doorsteps not through headlines alone, but through rising fuel costs, surging bond yields, and a quiet but meaningful tightening of mortgage credit — all landing on a housing market that was only just beginning to find its footing after the corrections of 2022–25.

What Is Actually Happening

The conflict began on February 28, 2026. Within weeks, Iran's closure of the Strait of Hormuz — through which roughly 20% of the world's seaborne oil supply normally passes — triggered the largest global energy supply disruption on record. Brent crude, which started the year near $70 per barrel, surged above $110 and has been hovering near that level since mid-March.

The Bank of Canada held its overnight rate at 2.25% at its March 18th announcement — an important signal of restraint. But the bond market, which sets fixed mortgage rates independently of the BoC's policy rate, has already moved. The sudden 30-basis-point jump in five-year fixed rates this week is what economists describe as an "accidental tightening" of monetary policy: credit conditions are tightening even though the BoC hasn't pulled the trigger.

For buyers already stretching toward their stress test ceiling, that 30-basis-point move is not abstract. On a $1 million mortgage, it can reduce maximum purchase qualification by $25,000–$40,000 — effectively removing a segment of the buyer pool from the most competitive price points.

What History Tells Us

Energy shocks and their downstream effects on housing markets are not new phenomena. Canada has lived through five major oil price crises since 1973, and each one left a distinct fingerprint on real estate. The nature of the shock, its duration, and — critically — how central banks responded all determined the severity of the housing impact.

Across all five episodes, the research confirms the same sequencing: sales volumes fall within 60–90 days of the shock, and price adjustments follow 3–9 months later. We are currently in the volume-freeze phase. The price evidence will arrive in the data later this year.

The "Commuter Tax" and What It Means for Suburban Demand

Beyond mortgage rate mechanics, high gas prices introduce a secondary pricing force with a specific geographic character. Research examining Canadian Census Metropolitan Areas from 1986–2006 found that for every 10% increase in gas prices, home values in high-commute areas typically see a 0.3%–0.4% relative decline compared to transit-accessible urban locations.

During the 2008 oil spike, "exurban" markets — those further from the core than Oakville — were the first to see sales volume fall. Buyers began calculating a "fuel-adjusted mortgage payment," treating the monthly cost of commuting as a fixed debt obligation stacked on top of their mortgage.

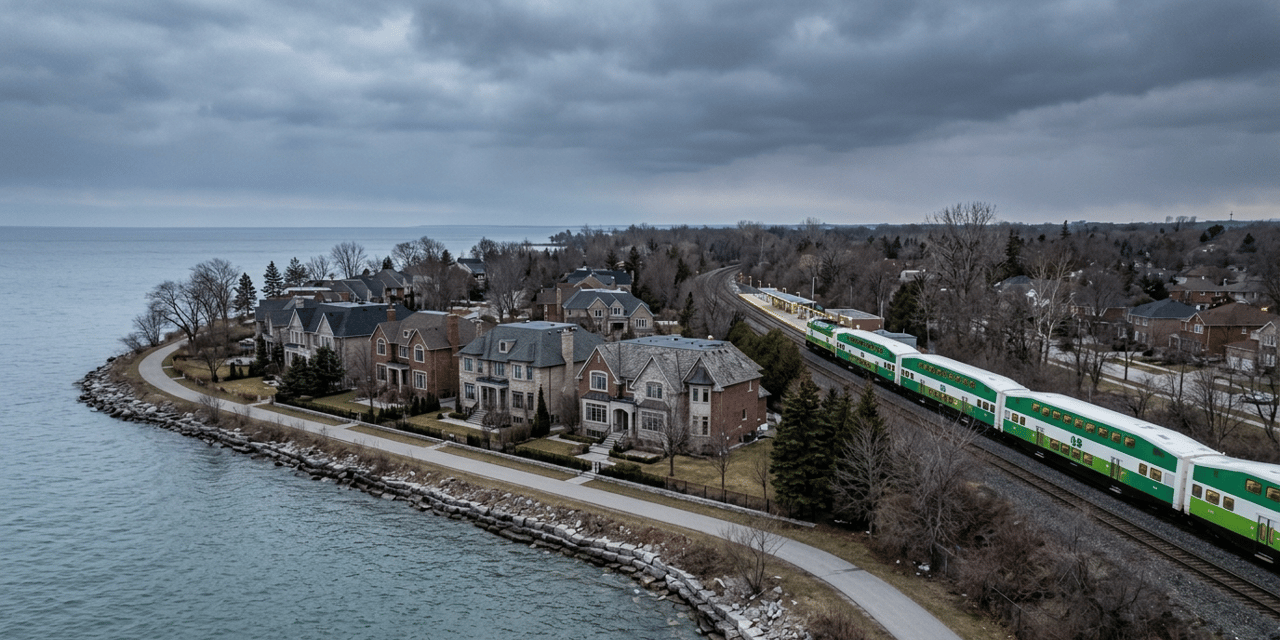

Oakville's Structural Advantages

Unlike deeper "drive-until-you-qualify" communities, Oakville has two durable protective factors that historical data consistently validate as shock absorbers:

- GO Transit connectivity. When gas prices spike, demand for homes within a 10-minute radius of Oakville's and Bronte's GO stations has historically been measurably stickier than demand in car-dependent pockets. The commuter-rail hedge is real and quantifiable.

- Affluence and fundamentals-driven demand. Oakville's buyer profile — typically equity-rich, income-stable professionals — means purchasing decisions are driven more by lifestyle fundamentals (schools, waterfront, walkability, community quality) than by the literal monthly cost of filling a tank. These buyers are more sensitive to portfolio sentiment and market confidence than to fuel economics.

- Genuine supply scarcity in premium pockets. In Old Oakville and the established south-end, the supply of quality detached homes does not expand during a downturn. Scarcity protects value. A nervous market doesn't create new inventory in heritage neighbourhoods.

The segments most exposed to this environment are condos, townhomes in North Oakville, and car-dependent properties at the margin of affordability. These tend to move 2–3 times more than the detached heritage market in either direction.

The 30-Basis-Point Jump: Psychological and Financial

A 0.30% rise in a single week is a sticker-shock event. It functions differently from a gradual, well-telegraphed rate cycle — buyers have not had time to adjust expectations or recalibrate their search parameters.

For buyers near their stress test ceiling, this week's move reduces maximum purchase qualification by approximately $25,000–$40,000 on a $1 million mortgage — enough to shift a buyer from the detached segment into townhomes, or from townhomes into condos.

Historically, sudden rate spikes produce a 90-day "freeze" in sales volume. Buyers don't disappear — they pause to determine whether this is a temporary blip or the start of a new direction. Given active peace negotiations between Washington and Tehran, that determination may come quickly.

In the early 1990s and again in 2022, rising rates also triggered a brief surge of pre-approval buying — buyers rushing to close on locked-in lower rates — followed by a sharp volume drop once those locks expired. A similar pattern may emerge over the coming weeks.

Three Scenarios for the Rest of 2026

Outcomes for Oakville's market over the next 6–12 months will be largely determined by one variable: the duration of the conflict and whether the BoC is eventually forced to raise rates in response to sustained inflation.

What This Means If You're Buying or Selling in Oakville Today

For Sellers

The easy 3% gain that was pencilled in for 2026 has become a working 3% gain. The window for aggressive pricing has narrowed, and the gap between "priced right" and "priced aspirationally" is now consequential. Historically, the first 90 days after a shock is when properly priced, well-prepared properties still sell — and overpriced ones absorb the full duration of buyer hesitation.

Oakville's premium heritage properties — particularly detached freehold south of the QEW — retain the best relative positioning in all three scenarios. But even in this segment, buyers today have more time, more options, and more leverage than they did six months ago. Presentation, condition, and pricing precision matter more than they have at any point since late 2022.

For Buyers

A nervous market is often a buyer's market in disguise. In every historical cycle studied, buyers who moved during the uncertainty period — rather than waiting for the "all clear" — consistently outperformed those who paused. The all-clear never arrives cleanly; by the time it does, prices have already recovered.

If your financing is in order and your timeline is 5+ years, the current environment — more supply, longer days on market, negotiating leverage, and conditions once again acceptable — represents real opportunity in Oakville's detached segment. Variable-rate mortgages, currently available as low as 3.35%, may be the right vehicle for buyers who believe the BoC's next move is a cut rather than a hike.

The Variable That Matters Most

Watch the Bank of Canada, not the oil price. Every historical episode confirms that central bank rate policy determines how badly housing is damaged — not oil prices alone. Oil at $110 with a BoC holding at 2.25% is manageable. Oil at $110 with a BoC hiking toward 5% is a housing correction. Governor Macklem's explicit restraint on March 18th is the single most housing-protective signal of the month. Monitor every subsequent inflation print and BoC communication closely — that is your leading indicator for what comes next.

Oakville's Enduring Fundamentals

Gas prices change. Wars end. Bond yields settle. What doesn't change are the reasons people choose to build their lives in Oakville: the school system, the waterfront, the community quality, and the proximity to the economic centre of the country. Historically, Oakville has been among the first markets to recover after energy-led downturns precisely because these fundamentals are permanent. They are not priced away by a conflict. They are the floor.

This analysis is provided for informational purposes and reflects market conditions as of March 2026. It does not constitute financial or investment advice. Data sourced from CREA, Bank of Canada, Wikipedia (Economic impact of the 2026 Iran war), Al Jazeera, CNBC, NPR, and academic research on Canadian housing markets. All real estate decisions should be made in consultation with a qualified professional. Profit from our experience — The Martin Group, themartingroup.ca, 905-338-2083.