The Direct Answer: Maximize Your Down Payment in Oakville

In 2026, first-time buyers can combine the First Home Savings Account (FHSA) with the RRSP Home Buyers’ Plan (HBP) to access a powerful tax-free down payment. By maximizing both, an individual can leverage up to $100,000 ($40,000 from the FHSA plus $60,000 from the RRSP), plus any investment growth within the FHSA. For couples, this total jumps to $200,000, providing a significant advantage in the competitive Oakville market.

The Deep Dive

The FHSA has become a cornerstone for young professionals in the Halton Region, offering the unique "double-benefit" of tax-deductible contributions (like an RRSP) and tax-free withdrawals (like a TFSA). Unlike the HBP, which is essentially an interest-free loan from your retirement savings that must be repaid over 15 years, the FHSA does not require repayment. This makes the FHSA the priority vehicle for most North Oakville condo seekers.

Strategically, the most effective way to enter the market is to "stack" these programs. Many savvy buyers are now utilizing the HBP limit of $60,000 to supplement their FHSA savings. Because the FHSA allows for a $16,000 carry-forward limit if you opened the account in a previous year, high-income earners in Oakville often front-load these accounts to maximize compound growth before they even start their home search.

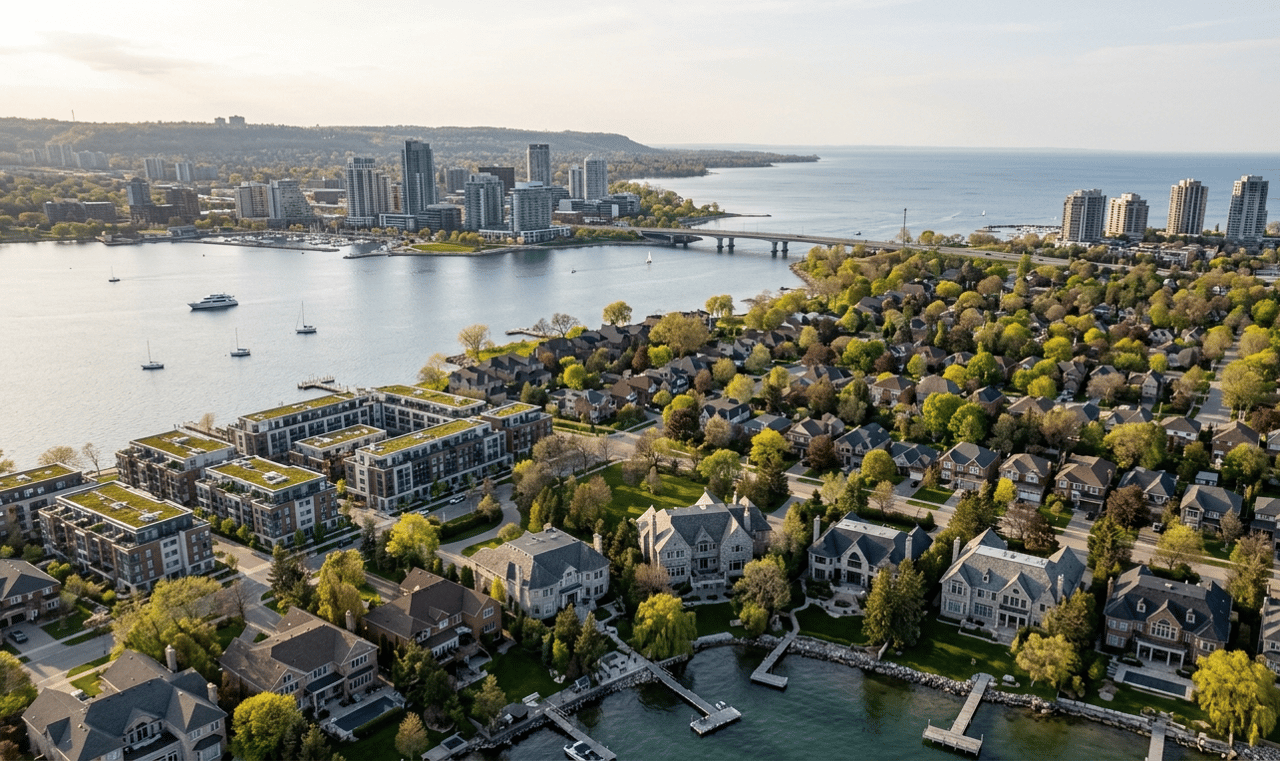

Local Nuance: The North Oakville Market

For the demographic targeting the modern mid-rise and high-rise developments in North Oakville—specifically near the Uptown Core and Dundas & Trafalgar—these tax-advantaged accounts are vital. With the 2026 average price for a condo apartment in Oakville sitting at approximately $715,000, a $100,000 combined down payment allows a single buyer to cross the 10% threshold comfortably, securing better mortgage rates and avoiding the higher premiums of low-down-payment loans.

Furthermore, buyers in areas like Joshua Creek or Glen Abbey should be aware that while the federal government has expanded the insured mortgage cap to $1.5 million, reaching a 20% down payment remains the gold standard to avoid CMHC premiums. Combining FHSA and HBP funds is often the most efficient way local first-time buyers bridge the gap for entry-level luxury townhomes, which are the "velocity leaders" of the 2026 market.

Key Takeaways for Oakville Buyers:

-

Total Access: Individuals can withdraw up to $100,000 (plus FHSA growth); couples up to $200,000.

-

No "Double Tax": FHSA withdrawals for a qualifying home are entirely tax-free and do not add to your annual income.

-

Repayment Nuance: HBP funds must be repaid starting the second year after withdrawal, while FHSA funds are yours to keep.

-

90-Day Rule: Remember that RRSP contributions must stay in the account for at least 90 days before an HBP withdrawal, whereas the FHSA has no such minimum holding period.

Work With the Oakville Experts

Navigating the intersection of tax policy and real estate requires precision. Whether you are looking for a sleek condo in Bronte or a family-starter in Glen Abbey, our team provides the data-driven insights and local expertise you need to win in today's "Strategic Equilibrium" market.

Contact Martin Group today to secure your future in the Halton Region.

"Profit from our experience."